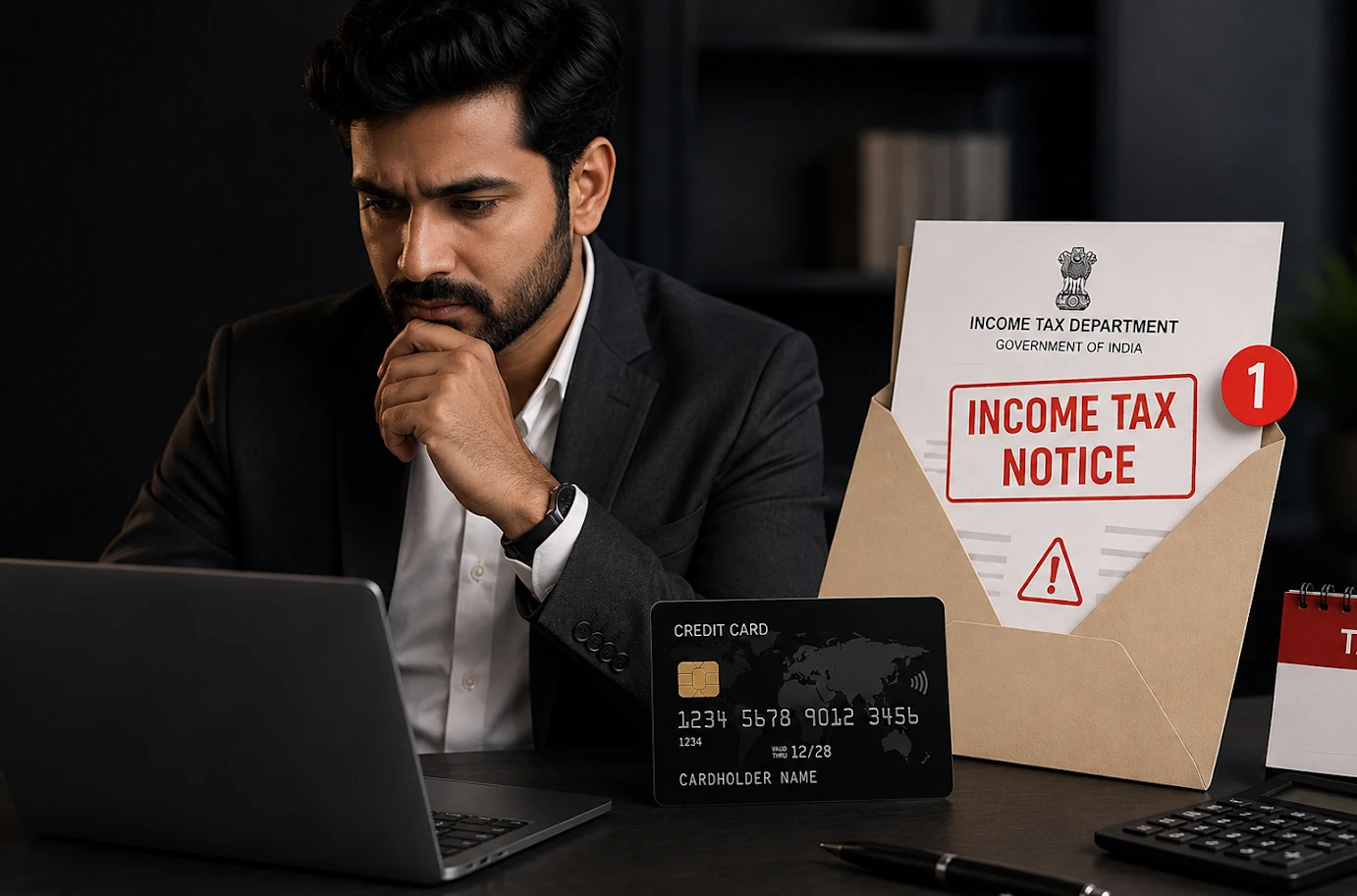

Can High-Value Credit Card Transactions Trigger an Income Tax Notice?

Paying for a luxury purchase, booking an international holiday, or settling a large business expense with your credit card has become part of everyday life for many Indians. As digital payments continue to grow, so does one common concern: Can a high-value credit card transaction attract the attention of the

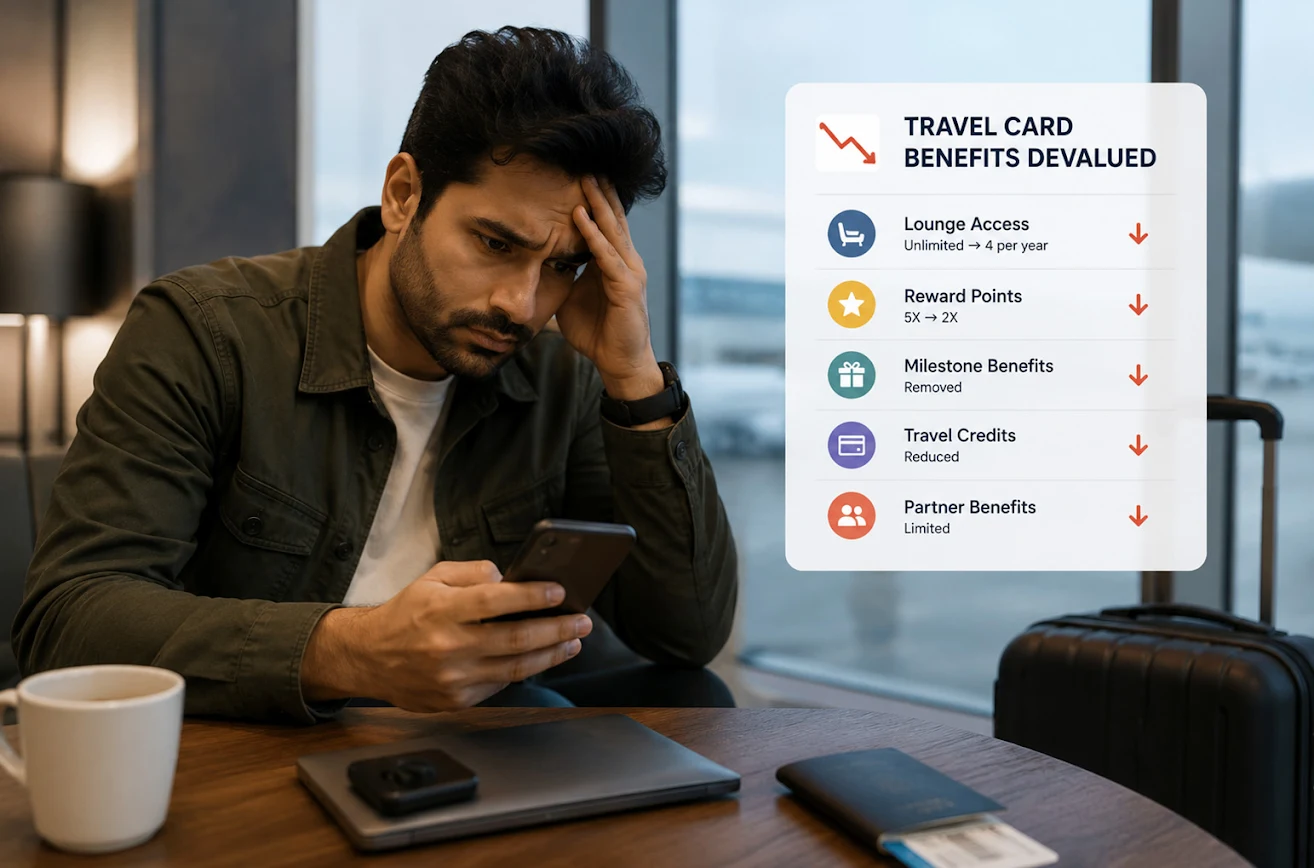

Why Are Travel Card Benefit Devaluations Increasing?

Travel credit cards were one of the slickest gadgets in the frequent traveler’s wallet for years. You may earn miles on regular spending, get access to airport lounges, benefit from travel advantages, and even get back the annual fee in rewards alone. It appeared to be a win-win for many

How Banks Track Your Spending Categories for Cashback: The Science of MCCs

Have you ever wondered how your bank magically knows that your Friday night swipe happened at a restaurant, not a retail store? You get your 5% reward instantly, while your friend using a different card gets a flat 1%. Knowing what’s going on under the hood with credit cards is